Are you one medical emergency away from financial disaster? Gap health insurance protects Americans facing devastating out-of-pocket costs that traditional plans don’t cover. Every year, millions discover their health coverage leaves dangerous payment gaps after accidents or serious illnesses strike. Medical debt remains the leading cause of bankruptcy, affecting over 530,000 American families annually according to the American Journal of Public Health. This comprehensive guide reveals how gap coverage health shields your savings, explains supplemental insurance mechanics, and helps you choose optimal protection. You’ll learn specific costs, enrollment strategies, and real-world examples demonstrating why gap health insurance becomes increasingly essential as healthcare expenses continue rising.

🎯 Key Takeaways

Gap health insurance bridges critical payment gaps between what your primary insurance covers and actual medical costs. These supplemental policies pay cash benefits directly to you when qualifying medical events occur.

Furthermore, they protect families with high-deductible plans from unexpected financial burdens. Meanwhile, premiums remain affordable compared to potential savings during medical emergencies. Ultimately, gap coverage health provides peace of mind and financial security simultaneously.

- 🎯 Key Takeaways

- What Is Gap Health Insurance?

- Gap insurance for health insurance

- How Gap Insurance Health Works

- Why You Need Gap Health Insurance

- Gap Health Insurance vs. Traditional

- Best Gap Coverage Health Plans 2025

- Gap Health Insurance Costs Explained

- Who Benefits from Gap Health Insurance

- Gap Coverage Health Enrollment Guide

- Common Gap Health Insurance Mistakes

- Gap Health Insurance Tax Benefits

- Real Stories: Gap Coverage Health Saves

- Future of Gap Health Insurance Trends

- Gap Health Insurance : Make your decision wisely

- FAQs

- Conclusion

- References

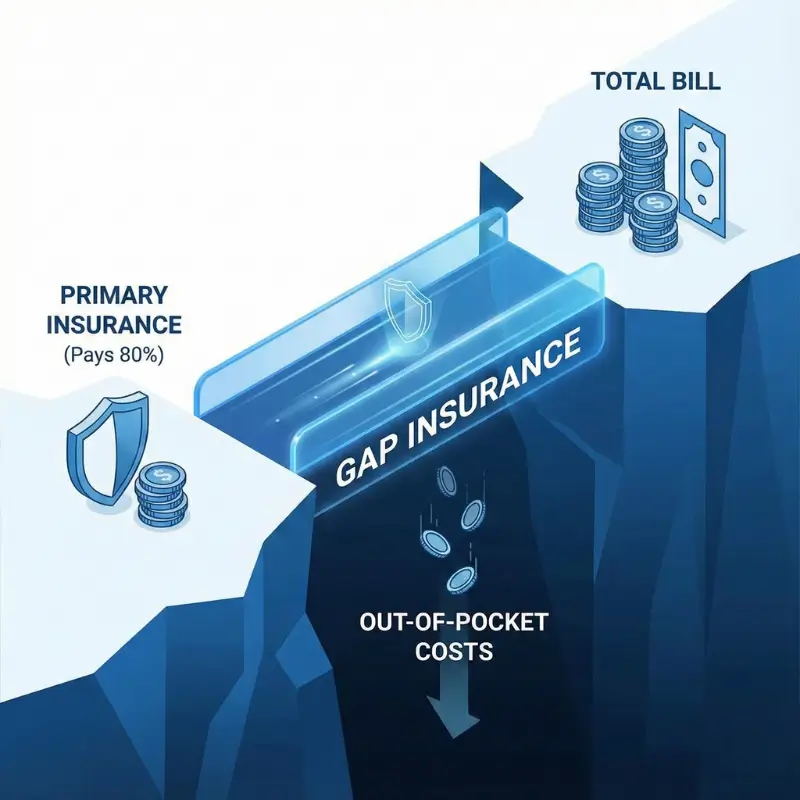

What Is Gap Health Insurance?

High deductibles leave you vulnerable

Modern health plans increasingly shift costs onto policyholders through elevated deductibles and copayments. The average family deductible reached $5,203 in 2024, according to the Kaiser Family Foundation. Consequently, many Americans delay necessary care because they cannot afford upfront expenses. Traditional coverage requires you to pay thousands before insurance activates fully. Moreover, coinsurance percentages mean you continue paying after meeting your deductible. Therefore, unexpected hospitalizations create immediate financial crises for unprepared households. Gap health insurance addresses these vulnerabilities directly and effectively.

Gap coverage health fills payment gaps

Supplemental policies specifically target expenses your primary insurance doesn’t cover completely or immediately. Gap coverage health pays benefits when you experience qualifying medical events like hospitalizations or surgeries. Additionally, these plans provide cash payments directly to policyholders rather than healthcare providers. This flexibility allows you to use funds for deductibles, copays, or even non-medical expenses. Furthermore, gap health insurance works alongside your existing coverage without replacement requirements. Subsequently, you maintain comprehensive protection across multiple financial exposure points. Therefore, combining both policy types creates robust healthcare security.

You avoid unexpected medical debt

Medical bills arrive quickly after treatment, demanding payment regardless of your financial readiness. Gap health insurance delivers cash benefits that prevent debt accumulation from qualifying healthcare events. Approximately 41% of Americans carry medical debt, totaling $195 billion nationwide per KFF research. Meanwhile, gap coverage health ensures you can pay providers promptly without draining emergency savings. Additionally, avoiding debt protects your credit score from damaging medical collection accounts. Consequently, your long-term financial health remains stable despite unexpected health challenges. Therefore, proactive gap health insurance prevents reactive debt management.

Gap insurance for health insurance

Traditional plans miss critical costs

Standard health insurance policies contain numerous coverage limitations that surprise policyholders during medical crises. Deductibles, copayments, coinsurance, and out-of-pocket maximums create substantial financial obligations before full coverage activates. Moreover, transportation costs to medical facilities remain uncovered by traditional plans entirely. Lost wages during recovery periods compound financial stress without supplemental protection mechanisms. Additionally, household expenses continue regardless of your ability to work after serious illnesses. gap insurance for health insurance specifically addresses these overlooked but significant financial burdens. Therefore, comprehensive protection requires multiple coordinated coverage layers.

Supplemental gap insurance covers more

These specialized policies expand protection beyond traditional insurance boundaries through targeted benefit payments. Gap health insurance typically covers hospital admissions, emergency room visits, surgeries, and diagnostic procedures. Furthermore, many plans include benefits for ambulance services, physical therapy, and specialist consultations. Cash payments arrive quickly, often within 48 hours of claim submission with proper documentation. Additionally, you control how to spend these funds without provider or insurer restrictions. Subsequently, gap coverage health adapts to your specific financial needs during medical emergencies. Therefore, flexibility distinguishes supplemental policies from rigid traditional insurance.

Your family gains financial protection

Healthcare expenses affect entire households, not just individual patients requiring treatment or hospitalization. Gap health insurance protects family budgets from catastrophic medical events that threaten financial stability. According to CNBC, 46% of Americans would struggle covering a $1,000 emergency expense. Meanwhile, average hospital stays cost $13,262 per admission based on recent industry data. Consequently, gap coverage health prevents families from choosing between medical care and financial security. Additionally, children benefit when parents maintain stable income and avoid bankruptcy from medical debt. Therefore, family-wide protection justifies gap health insurance investments.

How Gap Insurance Health Works

Medical bills exceed your deductible

Healthcare expenses accumulate rapidly during serious medical events, quickly surpassing typical deductible thresholds. Emergency room visits alone average $1,389 before any actual treatment costs, per Peterson-KFF analysis. Subsequently, imaging, laboratory tests, medications, and procedures add thousands more to total bills. Meanwhile, your primary insurance requires deductible payment before coverage begins reducing your obligations. Additionally, coinsurance percentages mean you continue paying portions of every subsequent charge. Consequently, total out-of-pocket costs often reach $10,000-$20,000 for significant medical events. Gap insurance health activates precisely when these expenses exceed your financial comfort.

Gap health insurance pays the difference

Once qualifying medical events occur, supplemental policies deliver predetermined cash benefits directly to policyholders. These payments don’t depend on actual expenses incurred, eliminating complicated reimbursement claim processes. Furthermore, gap coverage health pays benefits regardless of whether your primary insurance covers services. For example, hospital admission triggers a fixed payment, such as $1,000 per day. Additionally, surgical procedures might generate $5,000 lump-sum benefits upon completion and documentation. Subsequently, you receive funds to offset deductibles, copays, or any related expenses. Therefore, gap health insurance provides predictable financial support during unpredictable medical situations.

You receive immediate cash benefits

Speed distinguishes gap coverage from traditional insurance reimbursement processes that often take weeks. Most gap health insurance providers process claims within 2-5 business days after receiving complete documentation. Consequently, you access funds while bills arrive, preventing late payment penalties or collections. Additionally, direct payment to policyholders eliminates provider network restrictions or prior authorization requirements. Furthermore, you can use benefits for non-medical expenses like childcare, transportation, or mortgage payments. Subsequently, financial flexibility reduces stress during recovery periods when focus should remain on healing. Therefore, immediate cash benefits maximize gap health insurance value.

Why You Need Gap Health Insurance

One accident destroys your savings

A single unexpected medical event can deplete years of careful financial planning within weeks. The average American household maintains only $4,500 in emergency savings, according to Bankrate surveys. Meanwhile, severe injuries or sudden illnesses generate $20,000-$50,000 in out-of-pocket costs even with insurance. Consequently, families exhaust savings, max credit cards, and borrow from retirement accounts during crises. Additionally, 66% of bankruptcies link directly to medical expenses and related income loss. Gap coverage health prevents this devastating financial cascade through proactive protection. Therefore, small premium investments protect substantial accumulated wealth.

Gap coverage health protects your income

Medical events don’t just create bills, they eliminate earning capacity during recovery and treatment periods. The average worker loses 11 days of wages annually due to personal or family illness. Furthermore, serious conditions require months away from employment without disability insurance coverage. Meanwhile, household expenses continue requiring payment regardless of reduced income during medical crises. Additionally, gap health insurance provides cash that replaces lost wages while you recover properly. Subsequently, families maintain financial stability without forcing premature returns to work before full healing. Therefore, income protection represents a crucial but overlooked gap coverage benefit.

Peace of mind replaces constant worry

Financial anxiety about potential medical costs affects mental health and overall wellbeing negatively. Approximately 45% of Americans worry about affording healthcare if serious illness strikes suddenly. Moreover, this stress influences healthcare decisions, causing people to delay necessary treatment or skip medications. Conversely, gap health insurance eliminates uncertainty through guaranteed benefits for qualifying medical events. Additionally, knowing supplemental coverage exists reduces stress, allowing focus on prevention and wellness. Furthermore, financial confidence improves family relationships by removing a common argument source between partners. Therefore, gap coverage health delivers psychological benefits beyond mere financial protection.

Gap Health Insurance vs. Traditional

Standard plans leave dangerous holes

Traditional health insurance operates on cost-sharing principles that create significant policyholder financial exposure. Deductibles must be satisfied before most coverage activates, often requiring $2,000-$8,000 in upfront payments. Subsequently, coinsurance percentages mean you continue paying 10-30% of all subsequent covered expenses. Additionally, out-of-pocket maximums can reach $9,450 for individuals and $18,900 for families in 2025. Meanwhile, these limits reset annually, creating recurring exposure windows every calendar year regardless of claims. Furthermore, non-covered services fall entirely on patients without any insurance contribution whatsoever. Gap health insurance specifically addresses these dangerous coverage holes.

Gap coverage health adds safety layers

Supplemental policies don’t replace traditional insurance, they complement it through strategic coverage gap elimination. Gap health insurance activates when primary coverage leaves you with substantial financial obligations. Moreover, these plans provide fixed benefits regardless of actual costs, simplifying financial planning. Additionally, gap coverage health doesn’t require network provider usage, eliminating common insurance restrictions. Furthermore, benefits pay directly to you rather than providers, maximizing spending flexibility. Subsequently, combining both policy types creates comprehensive protection against medical financial disasters. Therefore, layered coverage strategies prove more effective than single-policy approaches.

Smart coverage prevents bankruptcy risk

Medical bankruptcy affects Americans across all income levels, not just low-earners without insurance. According to research, 72% of bankruptcy filers had health insurance when medical debt accumulated. Nevertheless, high deductibles and out-of-pocket costs still devastated their finances completely. Conversely, gap health insurance provides the additional financial cushion preventing bankruptcy during crises. Additionally, benefits arrive quickly enough to pay providers and prevent collection activities. Furthermore, maintaining good credit protects employment prospects, housing options, and overall financial health. Subsequently, gap coverage health represents bankruptcy insurance at affordable premiums. Therefore, prevention proves far cheaper than financial recovery.

Best Gap Coverage Health Plans 2025

Rising costs threaten your security

Healthcare expenses continue climbing faster than wages, increasing financial vulnerability for American families. Medical costs rose 4.6% in 2024, while wages grew only 3.8% during the same period. Furthermore, hospital prices have increased 42% since 2019 according to Health Care Cost Institute data. Meanwhile, employer-sponsored insurance passes more costs onto employees through higher deductibles and premiums. Additionally, inflation affects household budgets, leaving less available for unexpected medical expenses. Consequently, gap health insurance becomes essential rather than optional for financial protection. Therefore, securing coverage now prevents future financial devastation.

Top gap health insurance options compared

| Provider | Monthly Premium | Hospital Benefit | Surgery Benefit | Coverage Highlights |

| Aflac | $25-$75 | $1,000/day | $2,000-$5,000 | Extensive rider options, fast claims |

| Colonial Life | $30-$80 | $1,200/day | $3,000-$6,000 | Employer group discounts available |

| Allstate | $35-$90 | $1,500/day | $4,000-$7,000 | Accident-focused coverage options |

| MetLife | $28-$85 | $1,100/day | $2,500-$5,500 | Comprehensive wellness benefits included |

These gap coverage health plans offer varying benefit levels based on premium investments. Additionally, most providers allow customization through optional riders for specific needs. Furthermore, family coverage typically costs 40-60% more than individual policies.

You choose affordable comprehensive care

Selecting optimal gap health insurance requires balancing premium costs against potential benefit values. Most policies cost $300-$1,000 annually for individuals, depending on coverage levels and age. Meanwhile, a single hospital stay easily generates $10,000+ in out-of-pocket costs without supplemental protection. Consequently, gap coverage health delivers exceptional return on investment during medical emergencies. Additionally, many employers offer group rates that reduce premiums by 20-30% compared to individual policies. Furthermore, starting coverage while young and healthy minimizes costs through lower risk ratings. Therefore, proactive enrollment maximizes gap health insurance affordability and value.

Gap Health Insurance Costs Explained

Premiums seem overwhelming at first

Initial gap health insurance quotes might appear expensive when comparing to traditional policy premiums. However, supplemental coverage costs represent only 10-15% of primary insurance premiums typically. Moreover, monthly payments of $40-$100 provide substantial financial protection against catastrophic medical expenses. Additionally, premiums remain fixed for policy terms, preventing unexpected increases during coverage periods. Furthermore, most providers offer annual payment options with 5-10% discounts for upfront commitment. Subsequently, budgeting for gap coverage health becomes manageable with proper financial planning. Therefore, perceived expense diminishes when considering potential benefit values.

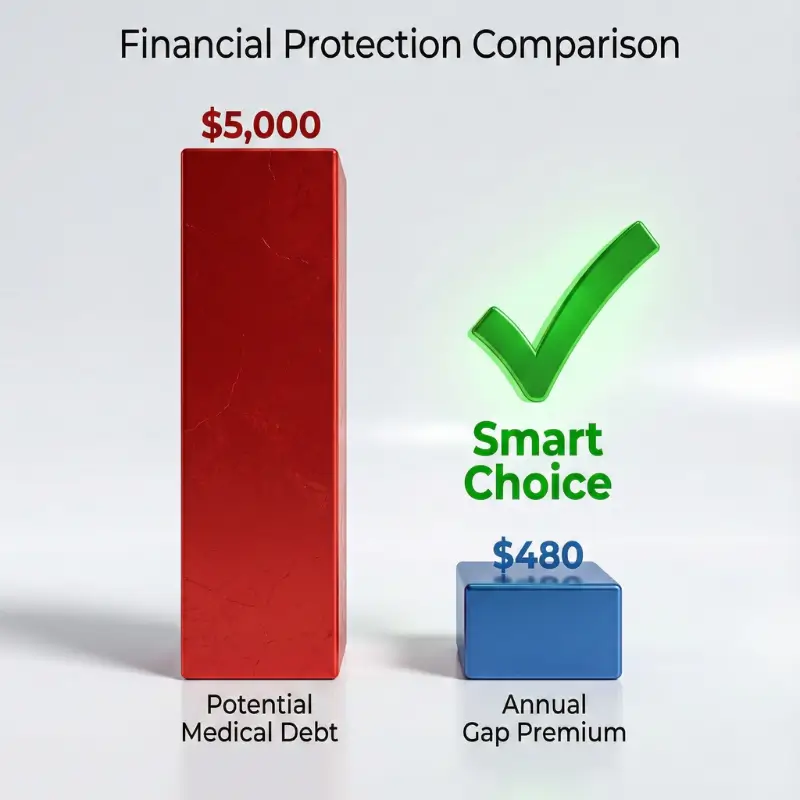

Gap coverage health pays for itself fast

A single qualifying medical event generates benefits exceeding years of premium payments immediately. For example, three-day hospitalization triggers $3,000 in gap health insurance benefits with typical policies. Meanwhile, annual premiums might total only $600, creating 5:1 benefit-to-cost ratios during claims. Additionally, multiple qualifying events within policy years compound return on investment significantly. Furthermore, avoiding medical debt prevents interest charges that would cost thousands over time. Subsequently, gap coverage health delivers measurable financial value during both claim and claim-free periods. Therefore, cost-benefit analysis strongly favors supplemental insurance investments.

Calculate your potential savings now

Personal Risk Assessment Formula:

| Current health insurance deductible: | $…………. |

| Average emergency room copay: | $…………. |

| Typical hospitalization duration: | ………. days × $1,200 = $…….. |

| Estimated surgical procedure cost: | $…………. |

| Total Potential Exposure: | $………… |

| Annual gap health insurance premium: | $…………. |

| Net Savings During Medical Event: | $………… (Line 5 – Line 6) |

This calculation reveals true gap coverage health value for your specific situation. Additionally, multiplying your deductible by two accounts for annual policy resets affecting ongoing conditions. Furthermore, considering family member risks increases total exposure and potential savings proportionally. Therefore, personalized calculations justify gap health insurance investments better than generic examples.

Who Benefits from Gap Health Insurance

High-deductible plans create major risks

Health Savings Account-qualified plans with $3,000-$7,000 deductibles attract many Americans seeking lower premiums.

However, these plans shift substantial financial risk onto policyholders during medical events. Moreover, 43% of workers now enroll in high-deductible plans, per Kaiser Family Foundation research. Meanwhile, most households cannot comfortably absorb $5,000+ unexpected expenses without financial hardship. Additionally, emergency situations prevent shopping for lower-cost care options when treatment becomes necessary. Consequently, gap health insurance becomes essential for high-deductible plan holders specifically. Therefore, premium savings disappear quickly without supplemental protection.

Gap insurance health suits these groups

✓ Families with young children: Accidents and illnesses occur frequently, generating multiple claims annually

✓ Self-employed individuals: Inconsistent income makes large unexpected expenses particularly devastating financially

✓ Pre-retirees (55-64): Higher medical risks before Medicare eligibility increases out-of-pocket cost probability

✓ Chronic condition patients: Ongoing treatment creates predictable but substantial annual out-of-pocket expenses

✓ Active lifestyle enthusiasts: Sports and physical activities increase injury risks requiring emergency care

✓ Limited savings households: Those without $10,000+ emergency funds face bankruptcy risks from medical debt

Gap coverage health provides targeted protection for these vulnerable populations specifically. Additionally, combination with existing coverage creates comprehensive financial security.

Families secure their financial future

Children’s unpredictable health needs create ongoing financial exposure for parents throughout childhood years. Emergency room visits for injuries or sudden illnesses occur an average 2.1 times before age 18. Furthermore, family deductibles double individual amounts, requiring $4,000-$10,000 before full coverage activates. Meanwhile, gap health insurance provides per-person benefits, multiplying protection for larger households proportionally. Additionally, protecting parental income and savings ensures children’s education funding and family stability long-term. Subsequently, gap coverage health represents an investment in family security beyond immediate medical expenses. Therefore, parents prioritize supplemental insurance as essential rather than optional.

Gap Coverage Health Enrollment Guide

Open enrollment deadlines approach fast

Annual enrollment periods typically occur October through December for coverage beginning January 1st. Missing these windows forces you to wait entire years before purchasing gap health insurance. However, qualifying life events like marriage, birth, or job changes create special enrollment opportunities. Additionally, some employers allow year-round supplemental coverage additions outside standard enrollment periods. Furthermore, individual market plans through providers like Aflac often permit enrollment anytime with immediate coverage. Nevertheless, planning ahead prevents gaps in protection during vulnerable transition periods. Therefore, mark enrollment deadlines prominently and prepare documentation early.

Easy steps to get gap health insurance

Enrollment Process:

- Assess needs: Calculate deductibles, out-of-pocket maximums, and potential medical expenses based on health history

- Compare providers: Review at least three gap coverage health carriers for benefits, costs, and reputation

- Request quotes: Obtain personalized premium estimates reflecting your age, location, and coverage preferences

- Review carefully: Understand benefit triggers, exclusions, waiting periods, and claim procedures before purchasing

- Complete application: Provide accurate health information and beneficiary designations during enrollment process

- Submit payment: Arrange automatic premium deductions to prevent coverage lapses from missed payments

- Confirm coverage: Verify policy activation dates and receive confirmation documents for records

This systematic approach ensures optimal gap health insurance selection and seamless enrollment.

Coverage starts protecting you immediately

Most gap coverage health policies activate within 24 hours of application approval and premium payment. However, some plans impose 30-90 day waiting periods for specific conditions or treatments. Additionally, accident-related benefits typically begin immediately without any waiting period restrictions whatsoever. Furthermore, pre-existing condition exclusions may apply for 6-12 months depending on specific policy terms. Nevertheless, gap health insurance provides immediate financial security against unexpected medical emergencies from enrollment. Subsequently, early enrollment maximizes protection duration and minimizes vulnerable exposure periods. Therefore, don’t delay coverage decisions until medical problems already exist.

Common Gap Health Insurance Mistakes

Assuming you’re fully covered hurts later

Many Americans mistakenly believe their primary health insurance provides complete financial protection against medical expenses. This dangerous assumption leads to devastating surprises when hospital bills arrive requiring thousands in payments. Moreover, understanding insurance terms like “deductible,” “coinsurance,” and “out-of-pocket maximum” proves challenging for consumers. According to studies, only 4% of Americans correctly define all four basic insurance terms. Consequently, gap coverage health becomes an afterthought rather than proactive protection strategy. Additionally, reviewing actual policy documents reveals coverage gaps that marketing materials obscure intentionally. Therefore, assume nothing and verify everything regarding insurance protection.

Avoid these gap coverage health errors

❌ Waiting until sick: Pre-existing conditions may be excluded, eliminating coverage when needed most urgently

❌ Choosing lowest premiums: Inadequate benefits fail to provide meaningful financial protection during claims

❌ Ignoring policy details: Misunderstanding benefit triggers and exclusions causes claim denials and frustration

❌ Forgetting to update: Life changes require coverage adjustments to maintain appropriate protection levels

❌ Skipping comparisons: Provider benefits and costs vary significantly, making research essential before purchasing

❌ Missing deadlines: Enrollment period lapses create coverage gaps exposing you to financial risks

Avoiding these mistakes ensures gap health insurance delivers intended protection when medical emergencies occur.

Smart choices save thousands annually

Informed gap coverage health decisions prevent both overpaying for coverage and underinsuring against real risks. Comparing multiple providers reveals $200-$500 annual savings opportunities for equivalent benefits and protection. Additionally, bundling supplemental policies with existing insurance carriers often generates 10-15% multi-policy discounts. Furthermore, selecting appropriate benefit levels based on actual risk assessment eliminates wasted premium spending. Subsequently, annual policy reviews ensure coverage remains aligned with changing health needs and circumstances. Moreover, maintaining continuous coverage prevents lapses that trigger new underwriting and potential exclusions. Therefore, strategic gap health insurance management maximizes value while minimizing costs.

Gap Health Insurance Tax Benefits

Medical expenses drain your budget

Healthcare costs represent an increasingly large portion of household budgets across all income levels. The average American family spends $8,435 annually on medical expenses including premiums and out-of-pocket costs. Furthermore, unexpected medical events can double or triple these costs during a single year. Meanwhile, most families don’t realize potential tax benefits that offset some healthcare expenses. Additionally, tracking all medical spending throughout the year requires organization that many households lack. Consequently, thousands of dollars in legitimate tax deductions go unclaimed annually across millions of families. The benefits associated with gap health insurance premiums interact with the tax code in a specific and advantageous way.

Gap coverage health offers deductions

Gap health insurance premiums may qualify as deductible medical expenses under specific circumstances and conditions. Self-employed individuals can deduct health insurance premiums, including gap coverage, directly from gross income. Additionally, employees can include premiums in itemized medical expense deductions if exceeding 7.5% AGI threshold. Furthermore, benefits received from gap health insurance typically don’t count as taxable income for recipients. Subsequently, you receive tax-free cash benefits while potentially deducting premium costs on returns. According to IRS Publication 502, qualified medical expenses include insurance premiums beyond employer-provided coverage. Therefore, gap health insurance creates favorable tax treatment compared to other financial protection strategies.

You maximize your tax savings legally

Tax Strategy Checklist:

✅ Track all gap health insurance premium payments with receipts and bank statements

✅ Document medical expenses exceeding 7.5% of adjusted gross income for itemized deductions

✅ Consult tax professionals about self-employment deduction eligibility and requirements

✅ Keep benefit payment records separate from medical expense documentation

✅ Consider HSA-compatible gap coverage if enrolled in high-deductible health plans

✅ Review state-specific tax treatments that may differ from federal regulations

Implementing these strategies ensures you capture all available tax benefits from gap coverage health investments. Additionally, proper documentation supports deductions during IRS audits or inquiries.

Real Stories: Gap Coverage Health Saves

Unexpected surgery caused financial ruin

Jennifer’s Story: This 34-year-old teacher faced emergency appendectomy requiring three-day hospitalization and surgical intervention. Her high-deductible health plan required $6,000 upfront before coverage activated despite paying $400 monthly premiums. Additionally, coinsurance meant she owed 20% of remaining $28,000 in total medical bills. Consequently, Jennifer faced $11,600 in out-of-pocket costs while recovering and unable to work. Furthermore, her modest emergency fund of $3,000 covered only a fraction of mounting expenses. Subsequently, Jennifer maxed credit cards, borrowed from family, and delayed mortgage payments during crisis. Medical debt destroyed her credit score, affecting future loan applications and employment background checks.

Gap health insurance rescued this family

Michael’s Experience: After purchasing gap coverage health costing $65 monthly, his teenage son broke his leg during soccer practice. The injury required surgery, hardware installation, and five days of hospitalization for complication monitoring. Traditional insurance left the family with $8,200 in deductibles, copays, and coinsurance obligations immediately. However, gap health insurance delivered $6,500 in benefits: $1,500 for surgery, $5,000 for hospitalization, covering most expenses. Additionally, benefits arrived within 72 hours of claim submission, allowing prompt provider payment. Consequently, Michael’s family avoided debt, maintained savings, and focused on their son’s recovery. Therefore, the policy paid for itself in a single event.

Now they recommend coverage to everyone

Both Jennifer and Michael share their experiences, emphasizing gap health insurance importance for financial protection. Jennifer now carries gap coverage despite additional monthly costs, calling it “financial insurance for my insurance.” Moreover, she educates colleagues about supplemental protection options during benefits enrollment periods each year. Meanwhile, Michael calculated that his family’s premiums totaled only $780 that year against $6,500 in received benefits. Additionally, avoiding $8,200 in debt saved thousands in credit card interest over subsequent years. Furthermore, both families maintain continuous gap coverage health, refusing to risk financial exposure again. Therefore, real-world experiences prove gap health insurance value beyond theoretical calculations.

Future of Gap Health Insurance Trends

Healthcare costs skyrocket every year

Medical expense inflation consistently exceeds general inflation rates, accelerating financial pressure on American families. Healthcare costs are projected to grow 5.4% annually through 2028 according to CMS projections. Meanwhile, wage growth predictions suggest only 3.1% annual increases during the same period. Consequently, the gap between earnings and medical expenses widens continuously, increasing financial vulnerability. Additionally, prescription drug costs rise faster than other healthcare categories, affecting chronic condition patients disproportionately. Furthermore, technological advances introduce expensive but life-saving treatments that insurance covers partially. Therefore, gap health insurance becomes increasingly essential rather than optional protection.

Gap coverage health becomes essential now

Insurance industry experts predict supplemental coverage markets will expand 40% by 2027 as consumers recognize protection gaps. Moreover, employers increasingly offer gap health insurance as voluntary benefits, acknowledging traditional coverage limitations. Additionally, younger generations demonstrate greater willingness to purchase supplemental protection after witnessing parents’ medical debt struggles. Furthermore, telehealth and digital enrollment platforms simplify gap coverage purchase and claim processes significantly. Subsequently, adoption rates among millennials and Gen Z exceed older generations by 60%. According to MarketWatch analysis, gap insurance markets show strongest growth among all supplemental coverage categories. Therefore, early adopters secure protection before inevitable premium increases.

Early adopters gain competitive advantages

Purchasing gap health insurance while young and healthy locks in lower premium rates permanently. Moreover, avoiding medical debt preserves credit scores that affect employment, housing, and loan opportunities. Additionally, financial stability during medical crises prevents career interruptions and lost advancement opportunities. Furthermore, comprehensive insurance knowledge distinguishes financially sophisticated individuals in competitive employment markets. Subsequently, employers value candidates demonstrating proactive risk management through supplemental coverage decisions. Moreover, maintaining continuous coverage prevents future exclusions for conditions developing after initial enrollment. Therefore, gap coverage health represents both immediate protection and long-term financial strategy.

Gap Health Insurance : Make your decision wisely

Confusion about coverage costs you money

Misunderstanding gap health insurance mechanics leads to suboptimal decisions that create financial vulnerability. Many consumers confuse supplemental policies with primary insurance, creating dangerous assumptions about protection levels. Additionally, comparing policies without understanding benefit structures results in inadequate coverage at excessive costs. Furthermore, industry jargon like “indemnity,” “fixed benefits,” and “supplemental” confuses average consumers significantly. According to research, 78% of Americans don’t fully understand their current health insurance coverage terms. Consequently, adding gap coverage complexity overwhelms decision-making processes, leading to inaction and continued exposure. Therefore, clear explanations eliminate barriers to essential financial protection.

You make informed confident decisions

Understanding gap health insurance mechanics empowers you to select optimal protection for specific situations. Armed with knowledge, you can compare policies effectively, negotiate employer-sponsored options, and budget appropriately. Additionally, recognizing how supplemental and primary coverage interact prevents dangerous assumptions about financial exposure. Furthermore, asking providers specific questions about benefit triggers, exclusions, and claim processes ensures transparency. Subsequently, informed consumers secure better coverage at lower costs through strategic policy selection. Moreover, confidence in coverage decisions reduces healthcare-related financial anxiety significantly and measurably. Therefore, education represents the first step toward comprehensive financial protection.

FAQs

What exactly does gap health insurance cover?

Gap coverage pays cash benefits when you experience qualifying medical events like hospitalizations, surgeries, or emergency treatments. These benefits help cover deductibles, copays, and other out-of-pocket expenses your primary insurance doesn’t fully cover.

Is gap health insurance worth the cost?

Yes, especially if you have high-deductible plans or limited emergency savings. A single medical event often generates benefits exceeding years of premium payments, providing excellent return on investment.

Can I use gap health insurance benefits for anything?

Benefits pay directly to you, allowing flexibility in spending for medical bills, lost wages, household expenses, or any financial needs during recovery.

When should I purchase gap coverage health?

Enroll during open enrollment periods or within 30 days of qualifying life events. However, many individual policies allow year-round enrollment with immediate accident coverage.

Does Medicare cover gaps in health insurance?

Traditional Medicare has coverage gaps, but Medigap policies specifically address those. Gap health insurance discussed here supplements working-age adults’ commercial insurance policies.

Will gap health insurance cover my family members?

Yes, you can purchase family policies covering spouses and dependent children, typically at 40-60% higher premiums than individual coverage.

Can my employer provide gap coverage health benefits?

Many employers offer gap health insurance as voluntary benefits with potential group discounts of 20-30% compared to individual market rates.

Does gap health insurance replace my regular health insurance?

No, gap coverage supplements existing insurance by paying benefits your primary plan doesn’t cover fully.

Can I purchase gap health insurance if I have pre-existing conditions?

Yes, though specific conditions may face exclusion periods of 6-12 months depending on policy terms.

How much does gap coverage health typically cost monthly?

Individual premiums range from $25-$90 monthly depending on age, location, and selected benefit levels.

Conclusion

Gap health insurance provides essential financial protection against devastating medical expenses that traditional coverage leaves exposed. High deductibles, copays, and coinsurance create substantial out-of-pocket costs reaching thousands annually for American families. Meanwhile, supplemental gap coverage delivers cash benefits that prevent medical debt, protect savings, and maintain financial stability. Furthermore, affordable premiums ranging from $300-$1,000 annually provide exceptional value during medical emergencies requiring hospitalization. Statistics demonstrate that medical debt causes over half of American bankruptcies despite insurance coverage. Therefore, gap health insurance represents crucial protection rather than optional luxury for comprehensive financial security. Take action today: compare providers, calculate your specific risk exposure, and enroll during the next available opportunity. Your family’s financial future depends on proactive protection decisions made before medical emergencies strike unexpectedly.

⚠️ Important Disclaimer: This article is for educational purposes only and should not be construed as legal, tax, or financial advice. Insurance regulations and tax laws are subject to change. Please consult with a licensed insurance agent, CPA, or Tax Attorney regarding your specific situation before making coverage decisions.

References

- American Journal of Public Health research on medical bankruptcy causes and statistics

- Kaiser Family Foundation’s 2024 employer health benefits survey covering deductible trends

- KFF analysis of Americans’ challenges with healthcare costs and medical debt

- CNBC reporting on healthcare costs squeezing American families’ budgets

- Peterson-KFF Health System Tracker on emergency room visit cost variations

- Bankrate survey data on American emergency savings levels and financial preparedness

- Health Care Cost Institute data on hospital price increases over time

- IRS Publication 502 covering medical and dental expense deduction guidelines

- CMS national health expenditure projections through 2028 for healthcare cost trends

- MarketWatch analysis of gap insurance market growth and supplemental coverage trends