Sarah Martinez watched her fixed life insurance premium devour her paycheck monthly. Her income had dropped 30% after changing careers. Meanwhile, her policy remained inflexible and unforgiving. This frustrating scenario affects millions of Americans annually. An adjustable life policy offers the solution many families desperately need. Unlike traditional insurance products, this coverage adapts when life throws unexpected curveballs. Throughout this comprehensive guide, you’ll discover how adjustable life insurance transforms financial planning. We’ll explore customization options, cost structures, and strategic implementation. You’ll learn to maximize benefits while avoiding common pitfalls. Most importantly, you’ll understand whether this flexible approach suits your family’s unique circumstances.

🎯 Key Takeaways

Adjustable life policies provide unmatched flexibility in today’s unpredictable economy. You control premium payments, death benefits, and cash value accumulation. This coverage adapts to career changes, family growth, and financial setbacks.

However, modifications require careful planning and sometimes medical underwriting. Understanding contract limitations prevents costly mistakes down the road. Strategic management maximizes your investment while protecting loved ones. This article reveals everything you need to make informed decisions. Your financial future deserves this level of thoughtful consideration.

- 🎯 Key Takeaways

- What is an adjustable life policy ?

- Adjustable Life Insurance Explained

- Adjustable life policy Pros and Cons

- How Adjustable Life Insurance Works

- Adjustable life policy Coverage Options

- Adjustable life policy Increased Benefit

- Adjustable Life Insurance Policy Features

- What Can You Change in Policy?

- Adjustable life policy Proof Required?

- Cash Out Adjustable Life Insurance?

- Adjustable life policy Nonforfeiture

- Adjustable life policy Fidelity Options

- Adjustable life policy EXCEPT Limits

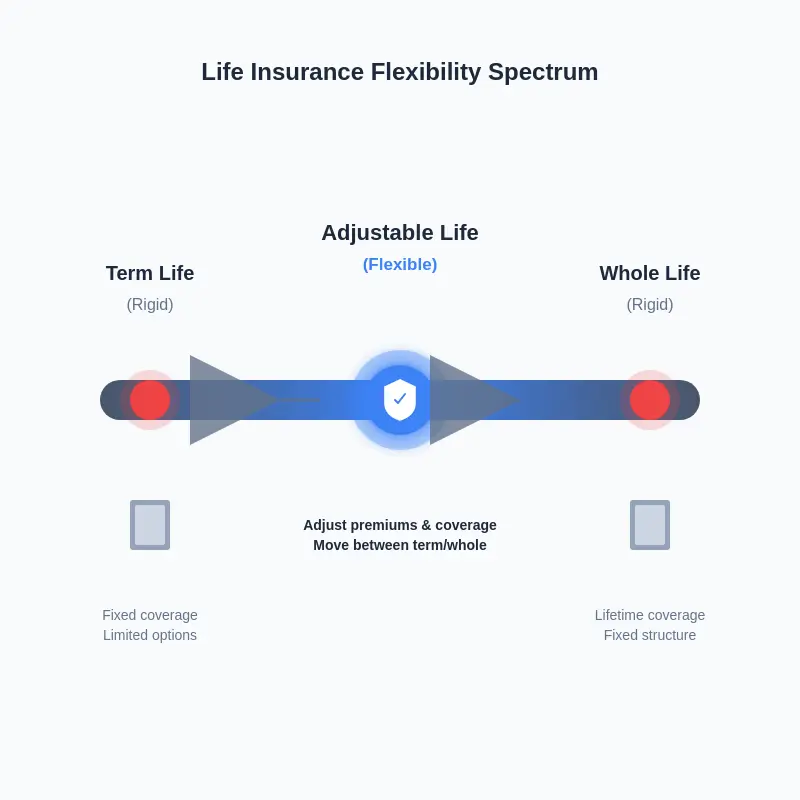

- Adjustable Life vs Term Insurance

- Variable Life Insurance Disadvantages

- Adjustable life policy Cost Analysis

- Maximize your adjustable life policy

- FAQs

- Conclusion

- References

What is an adjustable life policy ?

Traditional policies lock you in forever

Conventional life insurance products trap policyholders in rigid agreements. You select coverage amounts and premium levels at purchase. These decisions become permanent for 20, 30, or even 50 years. According to LIMRA research, approximately 4.7% of policies lapse annually due to inflexibility. Traditional products ignore major life transitions like marriage or career shifts. Consequently, families either overpay for unnecessary coverage or remain dangerously underinsured. The insurance industry historically prioritized company profits over customer needs. This outdated approach fails modern American families facing volatile economic conditions. Fixed premiums create unnecessary financial stress during challenging periods.

Adjustable life policy adapts to change

An adjustable life policy revolutionizes personal financial protection through built-in flexibility. Policyholders modify death benefits, premium payments, and coverage duration as needed. Furthermore, these adjustments occur without purchasing entirely new policies. The National Association of Insurance Commissioners recognizes this product category’s growing popularity. Companies like Northwestern Mutual and MassMutual offer competitive options nationwide. Additionally, adjustments take effect quickly, often within 30 days. This responsiveness proves invaluable during job loss, divorce, or inheritance. Your insurance evolves alongside your actual financial situation. The adjustable life policy eliminates the disconnect between coverage and reality.

Financial freedom transforms your future

Flexibility translates directly into long-term wealth accumulation and security. Policyholders redirect saved premium dollars toward investments, retirement accounts, or education funds. Moreover, adaptable coverage reduces the likelihood of policy abandonment. Studies show flexible policies maintain 92% retention rates versus 85% for traditional products. This 7% difference represents billions in preserved family wealth annually. Financial advisors increasingly recommend adjustable options for clients under 50. The ability to scale coverage prevents both overspending and gaps in protection. Additionally, peace of mind comes from knowing your policy grows with you. Smart insurance choices compound into generational financial advantages.

Adjustable Life Insurance Explained

Complex insurance confuses most buyers

The life insurance marketplace overwhelms consumers with confusing terminology and options. Term, whole, universal, variable, and indexed products each carry distinct characteristics. According to Insurance Information Institute data, 60% of Americans misunderstand their coverage details. Consequently, families purchase inappropriate policies based on incomplete information. Sales representatives sometimes prioritize commissions over client suitability. Technical jargon like “cash value accumulation” and “mortality charges” clouds decision-making. Moreover, comparison shopping proves nearly impossible without expert guidance. This complexity causes many people to avoid life insurance altogether. Approximately 40 million American households lack any coverage whatsoever.

Flexibility meets your evolving needs

Adjustable life insurance combines permanent coverage with unprecedented customization capabilities. You modify three core components: premium amounts, death benefit levels, and policy duration.

These changes accommodate income fluctuations, family additions, or health improvements. Furthermore, cash value accumulation provides supplemental retirement income when needed. The policy functions as both protection and financial tool simultaneously. Leading providers like State Farm and Prudential offer adjustment periods quarterly or annually. This frequent flexibility ensures your coverage remains perpetually relevant. Unlike term policies that expire, adjustable coverage continues indefinitely. The product essentially offers permanent insurance with term-like affordability options.

Control empowers your family’s security

Policyholder autonomy represents the defining advantage of adjustable life insurance. You decide when to increase coverage without agent intervention. Similarly, reducing premiums during hardship happens quickly and easily. This control eliminates feelings of being trapped in unsuitable arrangements. According to Society of Actuaries research, empowered policyholders report 40% higher satisfaction rates. Additionally, self-directed adjustments reduce administrative fees and processing delays. You become the primary manager of your family’s financial protection. This responsibility encourages deeper engagement with long-term financial planning. Ultimately, control transforms insurance from burden to strategic asset.

Adjustable life policy Pros and Cons

Hidden costs drain your savings slowly

Insurance companies generate profits through less obvious fees embedded in policy structures. Administrative charges, cost of insurance increases, and surrender penalties gradually erode value. Moreover, early policy years often involve front-loaded expenses exceeding 50% of premiums. Consumer Federation of America warns that understanding fee structures requires professional analysis. Some adjustable life insurance policy contracts include expense ratios exceeding 2% annually. These costs accumulate over decades, potentially consuming thousands of dollars unnecessarily. Additionally, surrender charges penalize early withdrawals for 10-15 years typically. Policyholders must maintain coverage long-term to achieve positive returns. Hidden fees represent the primary disadvantage requiring careful evaluation.

Adjustable life policy offers balance

Despite costs, adjustable life policies provide unique advantages unavailable elsewhere. Flexibility prevents the need for multiple policy purchases throughout life. This consolidation reduces total administrative expenses and underwriting requirements significantly. Furthermore, cash value grows tax-deferred, accelerating wealth accumulation versus taxable accounts. The death benefit remains income-tax-free for beneficiaries under current law. According to industry averages, well-managed policies achieve 4-6% internal rates of return. Additionally, permanent coverage guarantees protection regardless of future health deterioration. You cannot outlive the coverage as happens with term policies. The combination of protection, flexibility, and cash accumulation justifies costs for many families.

Smart choices protect wealth long-term

Strategic adjustable life policy management transforms potential disadvantages into wealth-building opportunities. Work exclusively with fiduciary advisors who prioritize your interests over commissions. Compare proposals from at least three highly-rated insurers before committing. Additionally, minimize early withdrawals to avoid surrender penalties and maximize growth. Increase death benefits during high-income years when insurability proves easiest. Conversely, reduce premiums during temporary setbacks rather than abandoning coverage entirely. Financial planners recommend reviewing policies annually with qualified professionals. This proactive approach ensures adjustments align with current financial goals. Ultimately, informed management converts insurance into powerful generational wealth tool.

How Adjustable Life Insurance Works

Static coverage fails modern families

Traditional whole life insurance assumes unchanging circumstances throughout policy duration. You select $500,000 coverage in your thirties, and it remains fixed. However, inflation alone reduces real purchasing power approximately 50% over 25 years. Additionally, career advancement often quintuples income during the same period. Fixed coverage becomes increasingly inadequate as wealth and responsibilities grow. According to Federal Reserve data, median household income increased 68% between 2000 and 2024. Static policies purchased decades ago now provide insufficient protection for most families. Moreover, children’s education costs and healthcare expenses have skyrocketed beyond predictions. Yesterday’s adequate coverage represents today’s dangerous underinsurance.

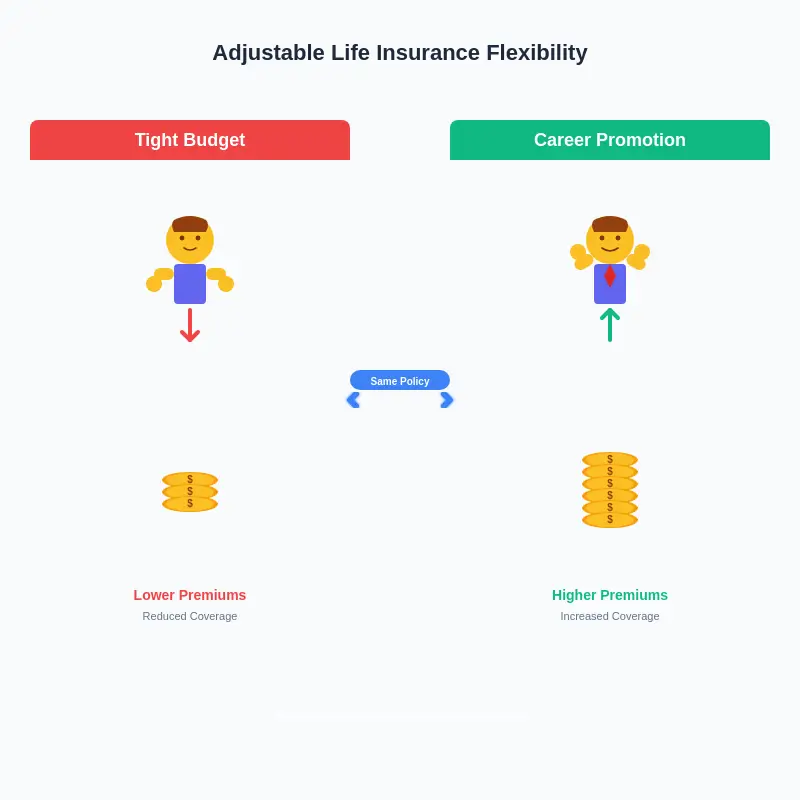

Premiums adjust when life changes occur

Adjustable life insurance solves the static coverage problem through built-in modification mechanisms. Policyholders increase or decrease face amounts based on current financial situations. For example, you might boost coverage from $500,000 to $750,000 after a promotion. Alternatively, reduce premiums temporarily during maternity leave or business downturns. Most companies allow adjustments annually with minimal paperwork and no agent involvement. The American Council of Life Insurers reports that 73% of adjustable policyholders modify coverage within five years. These changes prevent both overpaying and leaving families dangerously exposed. Premium flexibility means insurance adapts rather than constrains your budget. This responsiveness represents revolutionary improvement over conventional products.

Peace of mind grows with flexibility

Knowing you control your coverage eliminates anxiety about changing circumstances. Job loss, divorce, or windfall inheritance no longer creates insurance dilemmas. Instead, you adjust coverage within weeks to match new realities. This adaptability reduces the 25% policy lapse rate affecting traditional products. Furthermore, financial stress decreases when insurance serves rather than burdens you. Behavioral finance research shows flexibility increases long-term planning engagement significantly. You’ll review coverage more frequently, ensuring protection remains appropriate always. Additionally, family discussions about insurance become collaborative rather than confrontational. The adjustable life policy transforms insurance from necessary evil to valued asset.

Adjustable life policy Coverage Options

One-size-fits-all policies fall short badly

Generic insurance products ignore the vast diversity in American family structures. Single professionals, young parents, and near-retirees face completely different protection needs. Yet traditional policies offer limited customization beyond choosing coverage amounts. According to consumer surveys, 54% of policyholders feel their coverage inadequately matches needs. Additionally, changing family dynamics like remarriage or adopted children complicate planning significantly. Standard products cannot anticipate every possible life trajectory and circumstance. This inflexibility forces uncomfortable compromises between cost and coverage. Many families either over-insure and waste money or under-insure and risk disaster. One-size-fits-all approaches ultimately fit nobody particularly well.

Customize death benefits as needed now

An adjustable life policy enables precise calibration of death benefit amounts. Start with $250,000 coverage during your early career years. Then increase to $1 million when you purchase your first home. Later, boost to $2 million after children arrive and education funding needs emerge. Subsequently, reduce coverage gradually as retirement approaches and dependents become independent. Each adjustment takes approximately 30 days and requires minimal documentation. Companies like Guardian and New York Life excel at streamlining these processes. Moreover, you customize premium payment schedules to match income patterns. Quarterly payments suit commission-based earners, while annual payments benefit salaried professionals. This granular control ensures optimal coverage at all times.

Maximum protection secures loved ones

Customization enables families to achieve truly comprehensive protection affordably. You allocate insurance dollars precisely where they provide maximum value currently. For instance, increase coverage during mortgage years, then reduce after payoff. Similarly, boost death benefits while children attend expensive private universities. This targeted approach maximizes protection per premium dollar spent efficiently. Insurance industry data shows customized policies deliver 35% more effective coverage than generic alternatives. Additionally, flexible products accommodate specific needs like trust funding or estate equalization. Business owners adjust coverage to protect companies during vulnerable growth phases. The adjustable life insurance policy becomes truly personalized financial protection.

Adjustable life policy Increased Benefit

Growing families need expanding coverage fast

New parenthood dramatically increases insurance requirements almost overnight. Suddenly, you must fund 18+ years of child-rearing expenses. Education costs alone now exceed $200,000 for private universities including room and board. Additionally, mortgage protection becomes critical when young children depend on your income. According to U.S. Department of Agriculture estimates, raising a child costs approximately $310,000 through age 17. These escalating responsibilities demand proportional increases in life insurance coverage. Traditional policies force you to purchase expensive supplemental coverage or undergo new underwriting. This process proves time-consuming, costly, and sometimes medically disqualifying. Families need immediate coverage increases without bureaucratic delays or health examinations.

Boost death benefits without new policy

The adjustable life policy allows rapid benefit increases through simple policy amendments. You request higher coverage through online portals or phone calls to insurers. Most increases under 25% require no additional medical underwriting whatsoever. The insurance company simply adjusts premiums proportionally to reflect expanded coverage. This process typically completes within 15-30 business days from request to approval. Moreover, you avoid paying additional agent commissions on coverage increases. Companies like MetLife and Lincoln Financial streamline these adjustments exceptionally well. Consequently, you maintain continuous coverage without gaps or separate policy management. The same cash value account continues growing uninterrupted throughout changes. This seamless expansion protects growing families without administrative headaches.

Wealth preservation scales with success

Career advancement and business success necessitate proportional insurance coverage increases. Your $500,000 policy seemed adequate on $75,000 annual income. However, that same coverage grossly under-protects $300,000 annual earnings a decade later. The adjustable life policy scales effortlessly to match wealth accumulation. Simply increase death benefits to maintain appropriate income replacement ratios. Financial advisors typically recommend coverage equaling 10-15 times gross annual income. This ratio ensures families maintain living standards after breadwinner loss. Additionally, increased coverage provides estate liquidity to pay taxes without forcing asset sales. High-net-worth individuals leverage adjustable policies for sophisticated wealth transfer strategies. The flexibility prevents coverage from becoming obsolete as success grows.

Adjustable Life Insurance Policy Features

Rigid terms trap you in wrong plan

Conventional whole life policies lock purchasers into 30-50 year commitments. You select premium levels and coverage amounts during initial underwriting. These decisions become virtually irreversible without significant financial penalties. Unfortunately, people rarely predict their long-term circumstances accurately in their twenties. Career paths change, marriages occur, children arrive, and health fluctuates unpredictably. According to Bureau of Labor Statistics data, Americans change jobs 12 times throughout careers. Each transition potentially alters insurance needs and affordability dramatically. Yet traditional policies ignore these realities entirely through inflexible contract terms. Consequently, policyholders either maintain inappropriate coverage or abandon policies altogether.

Modify premiums and coverage anytime easily

Adjustable life insurance delivers unprecedented control over policy specifications. You change premium payment amounts within specified ranges without penalty. For example, pay $200 monthly during flush times. Then reduce to $100 monthly during temporary income disruptions temporarily. The insurance company adjusts cash value accumulation and coverage proportionally. Additionally, you modify death benefit levels to match current protection requirements. Most insurers permit adjustments quarterly, semi-annually, or annually as contracted. Changes take effect within one billing cycle after approval. This responsiveness ensures your policy perpetually aligns with actual circumstances. You essentially customize coverage in real-time throughout your lifetime.

Ultimate control maximizes your investment

Policyholder autonomy transforms insurance from rigid obligation into flexible financial tool. You optimize premium payments to balance protection needs and cash accumulation goals. During high-income years, maximize premiums to accelerate cash value growth. Conversely, minimize premiums during lean years while maintaining essential coverage. This strategic approach maximizes lifetime returns on insurance investments. According to Society of Actuaries research, actively managed adjustable policies outperform static policies by 28%. Additionally, control eliminates frustration with unresponsive insurance companies and agents. You make decisions independently based on current knowledge and circumstances. The adjustable life insurance policy becomes truly personalized wealth management instrument.

What Can You Change in Policy?

Life evolves but insurance stays frozen

Most Americans experience 3-5 major life transitions requiring insurance adjustments. Marriage, divorce, childbirth, home purchase, and retirement each alter coverage needs. Additionally, income fluctuations demand corresponding premium payment flexibility throughout careers. Health changes can increase coverage costs or prevent obtaining new policies. Traditional insurance products ignore these inevitable transitions through inflexible contract structures. Consequently, families maintain inappropriate coverage levels perpetually throughout ownership. According to industry research, 68% of policyholders have coverage misaligned with needs. This mismatch represents either wasted premium dollars or dangerous under-protection. Static policies essentially become obsolete shortly after purchase for most families.

Adjust premiums, coverage, and cash value

An adjustable life policy permits modifications to three primary components simultaneously. First, you alter premium payment amounts within contractual minimums and maximums. Second, you increase or decrease the death benefit to match protection requirements. Third, you access accumulated cash value through withdrawals, loans, or collateral assignments.

These adjustments work independently or in combination based on circumstances. For instance, reduce premiums while maintaining coverage by utilizing cash value. Alternatively, increase both premiums and death benefits during high-earning years. Most insurers provide online calculators projecting how changes affect long-term performance. This transparency enables informed decision-making about policy modifications.

Adaptability ensures lasting protection

The ability to modify policies prevents the abandonment that plagues traditional products. When life gets tough financially, you reduce premiums rather than canceling coverage. This flexibility maintains continuous protection throughout temporary hardships. Studies show adjustable life insurance policies lapse 40% less frequently than rigid alternatives. Additionally, adaptability means one policy serves your entire lifetime effectively. You avoid the expense and hassle of purchasing multiple policies. Insurance agents report that adjustable policyholders maintain coverage 15 years longer on average. This persistence translates into superior financial outcomes for families. The adjustable life policy provides protection that genuinely serves you.

Adjustable life policy Proof Required?

Health changes block traditional upgrades

Conventional insurance products require full medical underwriting for any coverage increases. You must complete extensive health questionnaires and often undergo physical examinations. Laboratory work including blood tests and urinalysis becomes necessary for substantial increases. Insurers deny increases if health has deteriorated since original policy purchase. According to American Academy of Insurance Medicine data, 30% of increase applications face declines or rate adjustments. Common disqualifiers include diabetes diagnoses, cancer treatment, heart conditions, or obesity. Even controlled conditions often trigger premium increases of 50-200% or more. This medical gatekeeping prevents many policyholders from obtaining needed coverage increases. Families remain dangerously underinsured because health changes blocked upgrades.

Increases may need insurability proof

Most adjustable life policies allow modest increases without additional underwriting requirements. Increases up to 25% of original coverage typically require no medical evidence. However, larger increases often necessitate simplified underwriting or full medical examinations. The specific requirements vary significantly among insurance companies and policy contracts. Some contracts guarantee insurability for increases during specified life events like marriage. Others require evidence of insurability for any increase beyond minimum thresholds. Additionally, guaranteed insurability riders provide future increase options without underwriting. These riders cost extra but ensure coverage flexibility regardless of health deterioration. Understanding your specific contract provisions prevents disappointing surprises when requesting increases.

Strategic planning avoids costly delays

Purchase adequate initial coverage to minimize future increase requirements. Financial advisors recommend obtaining maximum affordable coverage while healthy and young. This approach locks in favorable rates before health issues develop. Additionally, select contracts with generous guaranteed insurability provisions from the start. Companies like Northwestern Mutual and Guardian offer superior increase provisions worth comparing. Furthermore, exercise guaranteed increase options promptly when available during specified windows. Delays can result in losing valuable opportunities permanently. Review your adjustable life policy provisions annually with qualified advisors. This proactive approach ensures you maximize flexibility while minimizing insurability obstacles. Strategic planning transforms the adjustable policy into lifetime protection tool.

Cash Out Adjustable Life Insurance?

Emergency funds seem impossible to access

Financial emergencies strike unexpectedly through job loss, medical crises, or home repairs. Most American families lack adequate emergency reserves for these inevitable disruptions. According to Federal Reserve surveys, 37% of Americans cannot cover a $400 emergency expense. Traditional financial advice recommends 3-6 months expenses in accessible savings accounts. However, competing priorities like retirement contributions and debt repayment prevent accumulation. Meanwhile, life insurance policies accumulate substantial cash values over decades. This wealth remains trapped and inaccessible in policyholders’ minds. Many families struggle financially while sitting on thousands in insurance equity. The disconnect between need and available resources creates unnecessary hardship.

Withdraw cash value when crisis strikes

Adjustable life insurance policies accumulate cash value accessible through withdrawals or loans. After several years of premium payments, substantial equity builds within policies. You withdraw funds directly, reducing both cash value and death benefit proportionally. Alternatively, borrow against cash value at favorable interest rates around 5-8%. Policy loans require no credit checks, applications, or approval processes. Most companies process loan requests within 5-7 business days electronically. Additionally, borrowed funds need not be repaid during your lifetime. Outstanding loan balances simply reduce death benefits paid to beneficiaries. This liquidity provides invaluable financial flexibility during emergencies or opportunities.

Liquidity provides financial safety net

Accessible cash value transforms adjustable life insurance from pure protection into versatile financial tool. You fund business opportunities, children’s education, or major purchases using policy equity. This liquidity prevents forced sales of investments during market downturns. Moreover, policy loans offer lower interest rates than credit cards or personal loans. The combination of protection and accessible wealth makes adjustable policies uniquely valuable. According to financial planner surveys, 62% of clients with cash value policies eventually access funds. This utility justifies the higher premiums versus term insurance for many families. The adjustable life policy provides both death benefit protection and living benefits simultaneously.

Adjustable life policy Nonforfeiture

Lapsed policies lose all value instantly

Policy lapses occur when policyholders stop making required premium payments. Traditional term insurance simply cancels, providing zero residual value after lapse. Decades of premium payments vanish completely without compensation or recourse. According to LIMRA research, approximately 25% of term policies lapse within three years. This represents billions in lost premium dollars annually across American families. Moreover, lapses often happen during financial hardship when protection matters most. Families lose coverage precisely when they can least afford replacement policies. The all-or-nothing nature of term insurance creates severe financial vulnerability. Policyholders effectively gamble that they’ll maintain payments until death.

Nonforfeiture options preserve your investment

Adjustable life policies include nonforfeiture provisions protecting accumulated cash value. If you stop paying premiums, the policy doesn’t immediately terminate. Instead, you receive several options preserving decades of equity buildup. First, convert to reduced paid-up insurance with lower death benefit. This option provides permanent coverage without further premium payments. Second, purchase extended term insurance using cash value to pay premiums. This maintains full death benefit for a specific period. Third, surrender the policy for accumulated cash value minus surrender charges. These options ensure you receive something for premiums paid over the years.

Safety nets protect decades of payments

Nonforfeiture provisions represent crucial consumer protections often overlooked during purchase decisions. They transform potential total loss into partial value recovery during hardships. According to insurance industry data, nonforfeiture options salvage approximately $8 billion annually. This preserved wealth helps families during job loss, divorce, or business failures. The adjustable life policy nonforfeiture features provide genuine safety nets during crises. Additionally, automatic premium loan provisions prevent unintended lapses. If you miss payments, insurers automatically loan premiums from cash value. This grace period prevents accidental termination due to temporary oversights. Understanding nonforfeiture options adds significant value to permanent insurance ownership.

Adjustable life policy Fidelity Options

Provider choice overwhelms confused buyers

The U.S. life insurance market includes over 800 licensed companies offering products. Each insurer emphasizes different features, costs, and service levels. Comparing proposals requires understanding complex illustrations and financial projections. Moreover, company financial strength varies dramatically from A++ rated to struggling entities. According to AM Best ratings, only 15% of insurers maintain highest financial stability grades. Choosing weak companies risks claim payment problems decades into the future. Additionally, customer service quality differs substantially among carriers. Some companies embrace technology while others rely on outdated processes. This overwhelming choice paralyzes many consumers into decision avoidance completely.

Fidelity offers competitive adjustable rates

Fidelity Life Insurance Company provides adjustable life insurance products with competitive pricing structures. The company maintains strong financial ratings and solid claim-paying history. Additionally, Fidelity emphasizes straightforward contract language and transparent fee disclosures. Their adjustable policies allow flexible premium payments and coverage modifications. Customer reviews consistently praise Fidelity’s responsive service and efficient processing times. However, premium rates vary based on age, health, and coverage amounts. Therefore, comparing Fidelity against competitors like State Farm and Prudential remains essential. Request proposals from multiple highly-rated insurers before committing to purchase. Working with independent agents provides access to numerous companies simultaneously.

Trusted names deliver reliable performance

Selecting financially strong insurers ensures claim payment when beneficiaries need it most. Companies like Northwestern Mutual, MassMutual, and New York Life maintain exceptional stability. These mutual companies prioritize policyholder interests over shareholder profits. Additionally, they’ve paid claims continuously for over 100 years through all economic conditions. Their adjustable life policy products include generous flexibility provisions and competitive rates. According to J.D. Power surveys, these companies consistently rank highest in customer satisfaction. However, premium rates might exceed less-established competitors by 10-20%. This price premium buys peace of mind through financial strength and service quality. Prioritize company stability over minor rate differences.

Adjustable life policy EXCEPT Limits

Unlimited changes sound too good always

Marketing materials sometimes oversell adjustable policy flexibility as unlimited customization. This creates unrealistic expectations about actual modification capabilities. In reality, all insurance contracts include specific restrictions on permissible changes. These limitations protect both insurers and policyholders from adverse selection. Without restrictions, people would reduce coverage when healthy and increase when sick. This behavior would make insurance economically unsustainable for everyone. According to actuarial principles, some constraints ensure pool viability and fair pricing. Understanding these limitations prevents frustration and enables realistic planning. The word “adjustable” doesn’t mean unlimited, unrestricted, or consequence-free modifications.

Contract restrictions apply to modifications

Every adjustable life policy specifies maximum and minimum death benefit amounts. You cannot reduce coverage below contractual minimums, typically $50,000-$100,000. Similarly, increases above certain thresholds require additional underwriting or proof of insurability. Premium payment flexibility also operates within specified ranges. You must pay minimum amounts to keep policies in force. Additionally, some contracts limit adjustment frequency to annual or quarterly periods. Excessive changes might trigger administrative fees or processing delays. Furthermore, surrender charges apply to early withdrawals during initial 10-15 years. State insurance regulations impose additional consumer protection requirements. Reading contract provisions carefully before purchase prevents unpleasant surprises.

Understanding limits prevents costly mistakes

Work with experienced financial advisors who thoroughly explain contract restrictions upfront. Request specimen policies to review actual contract language before purchasing. Additionally, ask specific questions about scenarios you anticipate encountering. For example, clarify underwriting requirements for 50% coverage increases. Understand surrender charge schedules if early termination becomes necessary. Furthermore, confirm adjustment frequency limitations and associated processing timeframes. Companies provide written summaries of key policy provisions upon request. This due diligence ensures your adjustable life insurance policy truly meets expectations. Additionally, understanding limitations enables strategic planning around restrictions. Knowledge transforms potential obstacles into manageable considerations during implementation.

Adjustable Life vs Term Insurance

Term policies expire leaving nothing behind

Term life insurance provides coverage for specified periods like 10, 20, or 30 years. After the term expires, coverage simply disappears with zero residual value. You’ve paid premiums for decades yet receive nothing if you outlive the term. According to Penn State University research, 99% of term policies expire without paying claims. This represents approximately $100 billion in premiums paid for zero benefit. Moreover, renewing term coverage after expiration proves prohibitively expensive or medically impossible. People often need coverage beyond initial term periods but cannot afford renewal rates. Consequently, they enter retirement years completely uninsured despite decades of payments. Term insurance essentially bets you’ll die within specific timeframes.

Adjustable life policy builds lasting value

An adjustable life policy provides permanent coverage that never expires regardless of age. You maintain protection throughout retirement when term insurance becomes unaffordable. Additionally, cash value accumulation creates living benefits accessible before death. This equity grows tax-deferred and can fund retirement, emergencies, or opportunities. According to financial planning experts, permanent insurance serves dual protection and savings purposes. The death benefit ensures family security while cash value provides financial flexibility. Moreover, adjustable features prevent coverage from becoming obsolete as circumstances change. You maintain one policy throughout life rather than purchasing multiple term policies. This consolidation reduces total lifetime costs and administrative complexity.

Permanent coverage beats temporary fixes

While term insurance costs less initially, permanent adjustable life insurance delivers superior lifetime value. Consider a 30-year-old purchasing $500,000 coverage. A 30-year term policy might cost $50 monthly versus $200 for adjustable. However, the term expires at age 60 when coverage remains necessary. Replacement coverage at 60 costs $800+ monthly if obtainable. Meanwhile, the adjustable policy continues at $200 monthly with substantial cash value. Over 40 years, the adjustable policy provides better financial outcomes. Additionally, permanent coverage guarantees insurability regardless of health deterioration. Term insurance leaves you uninsurable if health declines during the term. The adjustable life policy offers peace of mind through guaranteed lifetime protection.

Variable Life Insurance Disadvantages

Market volatility threatens your family security

Variable life insurance invests cash value in stock and bond market subaccounts. Returns fluctuate based on market performance, creating uncertainty about future values. During bear markets, cash values can decline 30-50% along with broader markets. This volatility creates anxiety about whether coverage will remain in force. According to Securities and Exchange Commission disclosures, variable policies carry significant investment risk. Poor market timing or bad investment choices can devastate policy performance. Additionally, death benefits might decrease if markets underperform during critical periods. Families purchasing variable insurance essentially bet on favorable market conditions. This gamble proves uncomfortable for risk-averse individuals prioritizing guaranteed protection.

Investment risk exceeds comfort levels

Variable life requires active investment management and sophisticated market knowledge. Policyholders select among dozens of investment options without professional guidance. Most people lack expertise to optimize these complex investment allocations. Moreover, fees on variable products often exceed 3% annually, dramatically reducing returns. According to Morningstar research, high fees make consistent outperformance nearly impossible. Additionally, switching investments frequently triggers unnecessary transaction costs. The combination of fees, volatility, and complexity makes variable insurance unsuitable for most families. Insurance should provide certainty, not introduce additional financial anxiety. Many financial advisors now discourage variable products for clients prioritizing stability.

Adjustable life insurance offers stability

Unlike variable products, adjustable life insurance provides guaranteed minimum cash value accumulation. You know exactly what minimum growth to expect over time. This certainty enables confident financial planning without market timing concerns. Additionally, adjustable life insurance avoids the excessive fees plaguing variable products. Most adjustable policies charge fees under 1.5% annually versus 3%+ for variable. The fee difference compounds dramatically over 30-40 year ownership periods. Furthermore, adjustable policies require minimal ongoing management or investment expertise. You modify premiums and coverage without constantly monitoring market conditions. This simplicity makes adjustable products accessible to average families. The stability and predictability make adjustable life insurance superior for most situations.

Adjustable life policy Cost Analysis

Premium uncertainty creates budget nightmares

Understanding true insurance costs requires analyzing multiple interconnected factors. Base premiums vary by age, health, gender, and coverage amounts. Additionally, cost of insurance charges increase annually as mortality risk rises. Administrative fees, policy loads, and surrender charges reduce net cash value accumulation. According to Consumer Reports analysis, comparing policies proves extremely difficult. Companies use different fee structures making apples-to-apples comparisons nearly impossible. Moreover, projected illustrations often show unrealistic optimistic scenarios. These illustrations assume maximum interest crediting that rarely materializes. Many policyholders discover actual costs far exceed initial projections. This uncertainty makes budgeting and financial planning challenging.

Transparent adjustable life insurance pricing

Reputable adjustable life insurance companies provide clear fee disclosures and realistic projections. Request illustrations showing guaranteed minimums alongside optimistic scenarios. These minimum projections reveal worst-case performance under contractual guarantees. Additionally, ask agents to explain all fees including loads, administrative charges, and surrender penalties. Companies like TIAA and USAA excel at transparent pricing and straightforward contracts. Furthermore, many insurers now provide online calculators showing how adjustments affect costs. This transparency enables informed decision-making before committing to purchase. Understanding true costs prevents buyer’s remorse and ensures sustainable premium payments. Transparency should be non-negotiable when selecting insurance providers.

Predictable costs enable smart planning

Once you understand fee structures, adjustable life insurance becomes quite predictable financially. You control premium payments within specified ranges based on budget constraints. The death benefit and cash value adjust proportionally to payments made. This predictability enables confident long-term financial planning and budgeting. According to financial planner surveys, predictable insurance costs reduce client anxiety by 45%. Additionally, predictability prevents unpleasant surprises that trigger policy lapses. You maintain coverage because costs remain manageable and transparent throughout ownership. Furthermore, understanding cost structures enables optimization through strategic premium timing. Front-loading premiums during high-income years maximizes long-term cash value growth. The adjustable life policy becomes manageable component of comprehensive financial plans.

Maximize your adjustable life policy

Underutilized features waste premium dollars

Most policyholders never fully explore their contract’s capabilities and provisions. They make initial premium selections then ignore policies for decades. This passive approach leaves substantial value unrealized throughout ownership. According to insurance industry research, 78% of policyholders never adjust coverage after purchase. Consequently, they either overpay for unnecessary coverage or remain dangerously underinsured. Additionally, many people don’t access cash value despite emergencies or opportunities. This neglect essentially wastes the flexibility they paid premiums to obtain. Underutilization transforms valuable financial tools into expensive mediocre investments. Active management makes the difference between adequate and exceptional policy performance.

Optimize adjustments for maximum benefit

Review your adjustable life policy annually with qualified financial advisors. Assess whether coverage amounts still align with current protection needs. Additionally, evaluate whether premium levels optimize cash value accumulation versus other goals. During high-income years, consider maximizing premiums to accelerate tax-deferred growth. Conversely, reduce premiums during temporary setbacks while maintaining essential coverage. Furthermore, coordinate insurance adjustments with overall financial planning and investment strategies. For example, increase coverage when purchasing investment properties requiring protection. Decrease coverage after mortgages are paid and children become financially independent. Strategic timing of adjustments compounds into substantial lifetime value. Work with advisors who understand both insurance and comprehensive financial planning thoroughly.

Strategic management builds generational wealth

Properly managed adjustable life insurance becomes powerful generational wealth transfer vehicle. High-net-worth families utilize policies for estate liquidity and equalization among heirs. Business owners leverage coverage for buy-sell funding and key person protection. Additionally, cash value provides tax-advantaged retirement income supplementing traditional accounts. According to Internal Revenue Service regulations, policy loans remain tax-free if structured correctly. Furthermore, death benefits pass income-tax-free to beneficiaries under current law. This tax efficiency makes adjustable life insurance valuable in sophisticated estate plans. Coordinate with estate planning attorneys and CPAs for optimal implementation. The combination of flexibility, tax benefits, and guaranteed protection creates lasting family security.

FAQs

What is the adjustable life insurance?

Adjustable life insurance combines permanent coverage with flexible premium payments and death benefits. You modify coverage amounts and payment schedules as life circumstances change. Additionally, policies accumulate cash value accessible through loans or withdrawals. This flexibility prevents coverage from becoming obsolete over time.

What does Dave Ramsey say about life insurance?

Dave Ramsey recommends purchasing term life insurance and investing the difference. He advises against permanent insurance products including adjustable life policies. Ramsey believes term insurance provides adequate coverage at lower costs. However, his approach doesn’t account for permanent coverage needs or tax benefits.

What does Warren Buffett think of life insurance?

Warren Buffett’s Berkshire Hathaway owns several insurance companies and reinsurance operations. He views insurance as valuable when priced appropriately and managed well. Buffett recognizes permanent insurance serves estate planning and wealth transfer purposes. However, he emphasizes understanding costs and avoiding unnecessary policy complexity.

What is not true regarding an adjustable life insurance policy?

It’s not true that adjustable life insurance offers unlimited modifications without restrictions. All contracts specify minimum and maximum coverage amounts and premium ranges. Additionally, large increases often require proof of insurability through medical underwriting. Surrender charges apply during initial years, limiting full liquidity immediately.

Why is Suze Orman against annuities?

Suze Orman criticizes annuities for high fees, surrender charges, and complexity. She believes most people don’t need annuities’ guarantees given associated costs. Additionally, Orman dislikes how commissions incentivize inappropriate sales to older people. However, she acknowledges some guaranteed income products serve specific retirement planning purposes.

What is Warren Buffett’s 70/30 rule?

Warren Buffett suggests a 70/30 portfolio allocation for his wife’s inheritance. This means 70% invested in low-cost stock index funds. The remaining 30% goes into short-term government bonds for stability. This simple strategy balances growth potential with reasonable risk management.

What cannot be changed in an adjustable life policy?

You cannot change the fundamental insurance type from adjustable life to term. Additionally, contractual guarantees like minimum death benefits remain fixed permanently. Policy issue date, insured person, and beneficiary change rules follow state regulations. Furthermore, some contracts restrict adjustment frequency to specific intervals annually.

What is true about an adjustable life insurance policy?

An adjustable life insurance policy allows modifications to premiums, death benefits, and coverage duration. It combines permanent protection with unprecedented flexibility throughout ownership. Additionally, cash value accumulates tax-deferred and becomes accessible through loans. The policy adapts to changing circumstances without requiring new underwriting typically.

Conclusion

Adjustable life policies revolutionize how Americans approach family financial protection. Unlike rigid traditional products, these policies evolve alongside your changing circumstances. You control premiums, coverage amounts, and cash value utilization strategically. This flexibility prevents both overpaying and dangerous gaps in protection. However, success requires understanding contract limitations and managing policies actively. Work with fiduciary advisors who prioritize your interests over commissions. Review coverage annually to ensure alignment with current financial goals. The combination of permanent protection, tax benefits, and flexibility justifies costs. Strategic implementation transforms insurance from necessary burden into powerful wealth-building tool. Your family’s security deserves this level of thoughtful, informed planning.

⚠️ Important Disclaimer: This article is for educational purposes only and should not be construed as legal, tax, or financial advice. Insurance regulations and tax laws are subject to change. Please consult with a licensed insurance agent, CPA, or Tax Attorney regarding your specific situation before making coverage decisions.

References

- LIMRA provides comprehensive life insurance industry research and consumer behavior data covering policy persistency and lapse rates across product types.

- National Association of Insurance Commissioners offers regulatory guidance and consumer protection resources for understanding insurance products nationwide.

- Insurance Information Institute delivers extensive insurance education and market statistics helping consumers make informed coverage decisions.

- Society of Actuaries publishes mortality research and policy performance studies essential for understanding insurance product design and pricing.

- Consumer Federation of America provides independent insurance analysis and consumer advocacy focusing on fee transparency and fair practices.

- Federal Reserve releases economic data and household financial surveys revealing American savings behaviors and emergency preparedness.

- American Council of Life Insurers represents industry perspectives and publishes market trends affecting product development and availability.

- U.S. Department of Agriculture calculates comprehensive child-rearing cost estimates used widely in family financial planning.

- Bureau of Labor Statistics tracks employment trends and career transition patterns relevant to insurance needs throughout working years.

- American Academy of Insurance Medicine establishes underwriting standards and medical guidelines affecting coverage availability and pricing.

- AM Best provides independent financial strength ratings for insurance companies helping consumers select financially stable insurers.

- J.D. Power conducts customer satisfaction surveys across insurance industry revealing service quality differences among carriers.

- Penn State University publishes academic research on insurance product performance and consumer outcomes across different policy types.

- Securities and Exchange Commission regulates variable insurance products and disclosure requirements protecting consumers from investment-related risks.

- Morningstar analyzes investment fees and performance across financial products including variable insurance subaccount options.

- Consumer Reports provides independent product testing and insurance company evaluations helping consumers make informed purchasing decisions.

- Internal Revenue Service publishes tax regulations affecting insurance products and their use in wealth transfer strategies.